Card issuing

To issue physical or virtual cards, Monext offers services and support ranging from ready-to-use solutions to fully tailored offers — in France and across Europe.

TECHNOLOGY

Easily manage your card lifecycle with REST APIs designed to integrate seamlessly with your systems — while meeting the expectations of end users.

EXPERTISE

Get support from our experts at every stage of your project.

SCALABILITY

From standard offers to custom solutions, our services evolve with your needs — and grow alongside your success.

our standard offer

Monext provides everything you need to launch your own physical and virtual card programs.

A SIMPLE OFFER WITH KEY FEATURES

Explore a wide range of features tailored to your activity:

- Virtual Cards

- 3DS

- PIN Selection and Reset

- Strong Authentication Hub

- Mobile Payement

- Usage Restrictions

- Webservices / API Rest

- Accounting FIles

- IHM

- Schemes : Mastercard, Visa

FOR PAYMENT INSTITUTIONS

Monext supports fintechs and neobanks in launching and managing their card programs.

- Benefit from a flexible and secure issuing platform.

- Rely on our ability to absorb rapidly growing volumes.

- Expand internationally with ease.

OUR TAILORED OFFER

For more specific needs or regulatory constraints, Monext knows how to adapt.

A SOLUTION DESIGNED FOR YOU

Whatever your needs or constraints, we offer custom functionality and support:

- Custom limits

- Fee & Commission Setup

- Offline Processing & Server

- Fraud Monitoring

- Personalized Flow

- Custom Card Files

- CB, Mastercard, Visa & Bancontact

FOR TRADITIONAL

& ONLINE BANKS

Our tailored services fit any type of bank. We support you throughout the full card lifecycle:

- Issuing Platform

- Balance Check

- Personnalization

- Opposition

- Activation

- PIN Selection

“At Keytrade Bank, Monext has established itself as an essential partner thanks to its Bancontact/VISA card issuing solution. Their responsive and high-quality support makes all the difference. Interactions with their teams are always clear, constructive, and results-oriented.”

BUSINESS OR PERSONAL CARDS:

MONEXT HAS THE SOLUTION

Professional Cards

Monext provides tailored solutions for business, corporate, and professional cards — including all the services needed to manage your card programs:

- Full lifecycle management (CMS)

- Pin by SMS, web etc.

- Authorization & Compensation Management

- Virtuals Cards

- Hierarchical and product-based spending limits

- Fraud Management

- Apple Pay & Google Pay Support

- PIN Selection & Changes

Personal cards

Monext’s solutions can handle highly specific use cases for private-label cards.

- Authorization rules by location, date and time

- Restrictions by type of goods and services

- Hierarchical and product-based spending limits

- Real-time monitoring

- Management of specific protocols

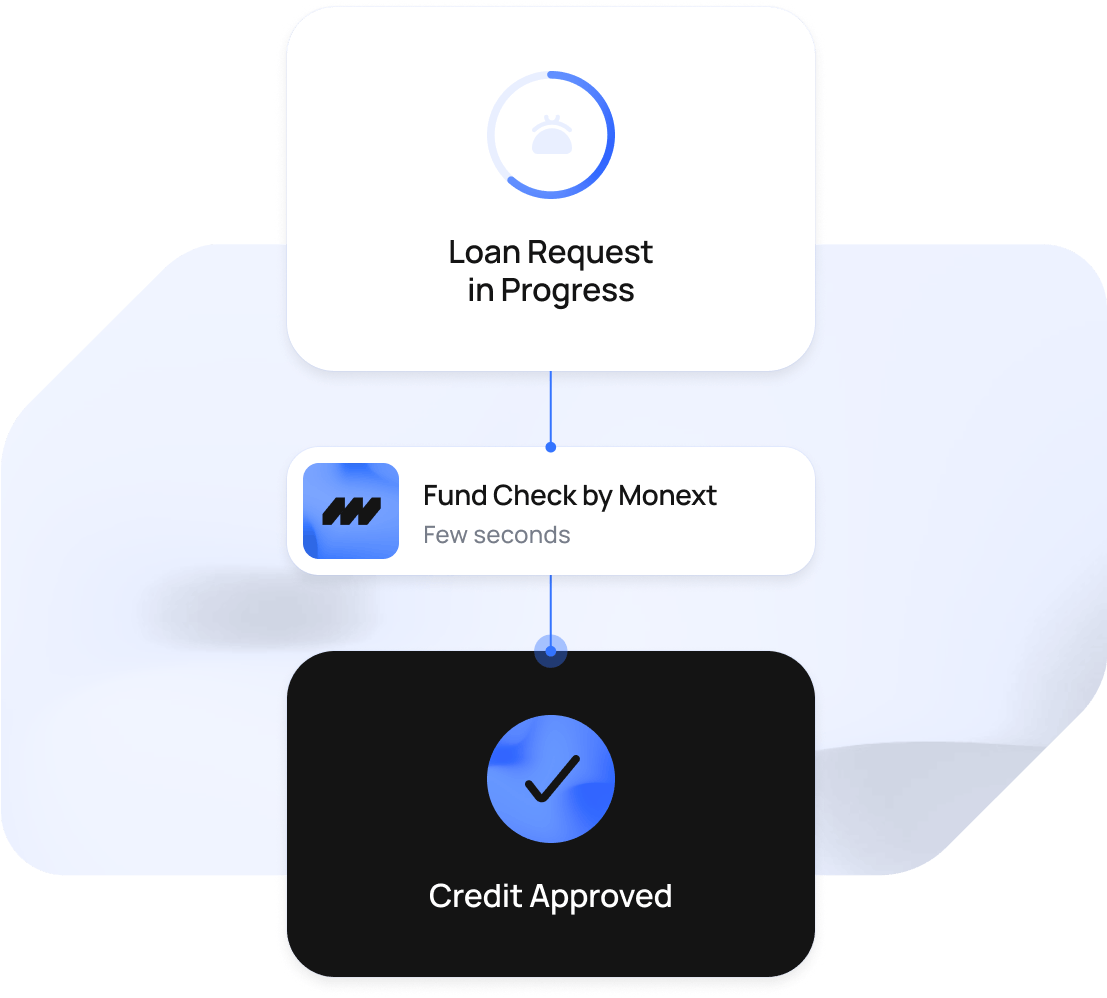

CREDIT SERVICES LINKED TO THE CARD

Cards are at the core of our credit solution. That’s why we offer a wide range of associated credit services:

- Assigned credit for in-store or online purchase financing

- Revolving credit for cards with a linked reserve

Self-care :

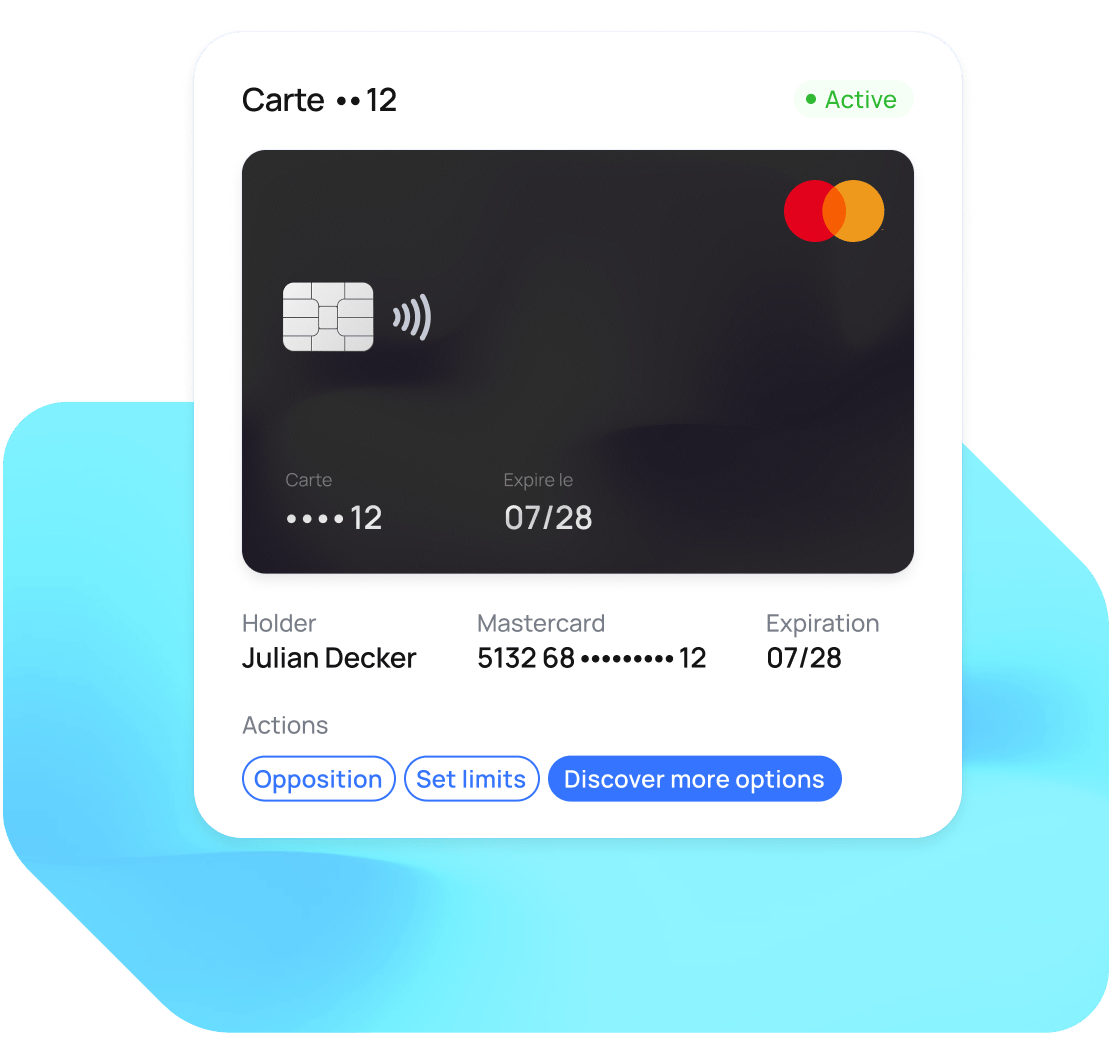

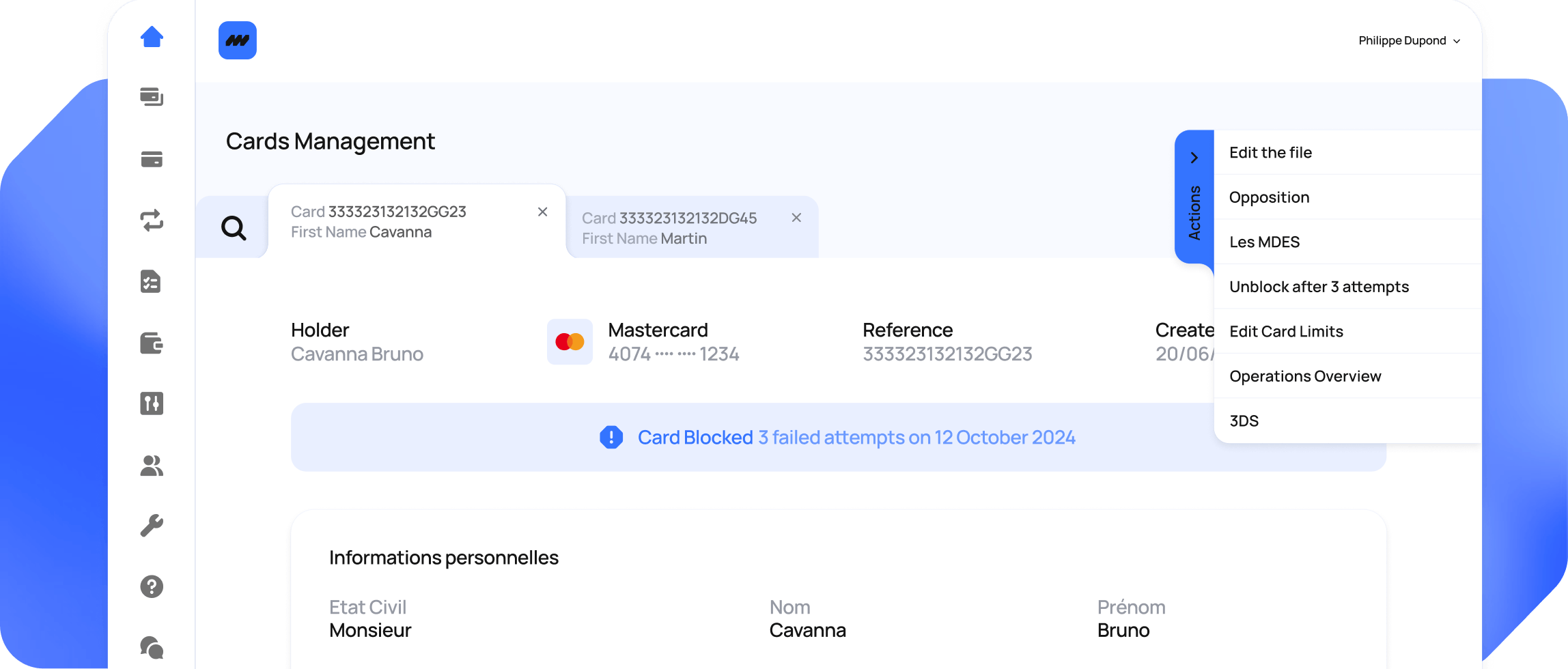

your back-office

Your customizable admin back-office, designed to simplify daily card management with complete autonomy.

Card management

Card actions

transactions monitoring

opposition

card re-issuing

pin management

temporary block

users management

FREQUENTLY ASKED QUESTIONS ABOUT CARD ISSUING

What is a card issuer?

A card issuer is a financial institution, a bank, a payment or electronic money institution which issues a bank card to a customer, who is the cardholder. The issuing of cards enables cardholders (customers) to make secure payment transactions, both in-store and on-line.

Card issuers may offer several uses and types of bank cards that meet their customers’ needs, in particular:

For everyday use: debit or credit cards, prepaid cards linked or not linked to a bank account.

For professional use: commercial cards which facilitate the management of expenses and the monitoring of transaction data for this specific activity.

These cards may be digital and found in mobile wallets such as XPay or simply through the generation of virtual cards to pay for on-line purchases safely.

The card issuer plays a key role in the management of the card programme, in payment security and in improving the customer experience.

What is the difference between card issuers and card networks?

Card issuers and card networks are two separate entities that have a complementary role in the payment card ecosystem.

🔹 Card issuers: Generally banks and financial institutions. They are responsible for issuing cards, managing cardholders and authorising transactions. They define the card ceilings, depending on the financial profile of the customer, offer credit functionalities through credit cards and ensure customer service through branches or apps.

🔹 Card networks (Carte Bancaire, Visa, Mastercard, Bancontact, etc.): they act as intermediaries between the various banks accepting card payments to merchants (acquiring banks) and the bank providing cards to their cardholders (issuing banks).

Card networks are based on two fundamental concepts: interbanking and universality.

They enable all cardholders to pay for purchases with any merchant.

What role does a card issuer play in the payment cycle?

Ultimately, the card issuer authorises the payment that their customers (cardholders) will make with a merchant or any company that accepts card payments. To be able to work, the card issued to the customer must be activated before being used.

The card issuer is involved in which functions?

Issuing the card: card generation, sending it to the customer (cardholder), activating it.

Payments: Payments can be broken down into two separate stages:

Authorisation: this phase takes place in real time when a customer makes a payment. The card issuer checks the validity of the account, in some cases the availability of funds or checks the expenditure ceiling, then authorises or rejects the transaction.

Clearing: this phase generally takes place at end-of-day, after the stores have closed. It involves receiving all the account movements to be recorded. The card issuer then debits its customers and pays the merchant’s bank (acquiring bank).

Throughout the card’s life cycle, the card issuer manages events related to the cardholder’s activity: payments, ceiling changes, digitalisation, upgrading of geographical checks. It also manages deferred payments, disputes and fraud prevention.

Why are card issuers so important for merchants?

The overwhelming majority of payments are made by card.

Card issuers who provide these cards to customers are a vital link in this cycle.

They ensure transaction security and authorise payments in accordance with each cardholder’s profile. They combat fraud by rolling out static rules and behaviour patterns in addition to strong authentication for their cardholders, ensure proper card acceptance and ultimately that merchants get paid.

By simplifying transactions and reducing risks, card issuers are strategic partners in merchants’ development.

Acquiring banks and card issuers: what’s the difference?

Card issuers and acquiring banks are two separate entities that interact through card networks to ensure smooth transactions.

Card issuer: this is the issuing bank or financial institution which provides a card to customers (cardholders). It manages card issues, authorises payments and also ensures that cardholders have sufficient funds.

Acquiring bank: this is the merchant’s bank. It is connected to the various on-line and in-store payment solutions which are used by the merchant. It accepts payment cards, processes transactions and ensures that merchants receive payment.

For example, when a customer pays for a purchase by card, the card issuer checks and authorises the transaction, while the acquiring bank receives the payment and transfers it to the merchant.

In short, the card issuer provides the payment card and authorises payments, while the acquiring bank enables merchants to accept and receive payments.

NO CONTACTLESS HERE

Our teams are always here to listen and assist with any questions, collaborations, or commercial inquiries.